RESEARCH RESEARCH

RESEARCH RESEARCHJuly 1998 CORPORATE PROFILE

CORPORATE BUSINESS DESCRIPTION

FUNDAMENTAL ANALYSIS

FUNDAMENTAL

ANALYSIS - Part 2

OVERVIEW

CORPORATE INFORMATION

FINAL

WORD

CORPORATE BUSINESS DESCRIPTION

The Company recycles plastics and non-ferrous metals it recovers from electrical/telephone components. SETO also recovers precious metals from circuit boards and obsolete computers. All recycling is done in Malaysia. It also manufactures plastic rope and rubber bands in Malaysia and Vietnam. The Company also sells to more than 400 customers disposable tools, including (1) diamond dicing blades and scribes which are the tooling components of precision electronic saws and scribers, (2) dressers for the shaping and forming of grinding wheels in the machine tool industry and (3) industrial ceramic products and clean room supplies.

Scrap Metal Recycling. Scrap metal recycling is done in the company's own facilities, which currently recycle 800 tons/month and has the capacity to recycle an additional 700 tons/month. The scrap is sourced locally in Malaysia and overseas through international networking, and the end products of the scrap metal recycling are processed scrap copper, cast-iron and aluminum.

Plastic Rope. The Company is the largest plastic rope manufacturer in Malaysia, with a 40% market share. It manufactures the rope from plastic resins (approximately 30% of which it obtains from its recycling operations), chemical composition and color pigments. It currently manufactures 350 tons of rope per month and has the capacity to produce an additional 150 tons per month. Rope sizes range from 2.5mm to 42mm for three or four-strand rope and from 3mm to 80mm for eight-strand braided rope (cross rope), rope length varies from 200m to 220m in coils and colors include white, black, green, yellow, blue and red.

New machinery along with an aggressive marketing strategy enabled the Company to expand into Australia, New Zealand and Europe. Import quotas have been a substantial obstacle preventing the Company from entering the United States market. However, in September 1997 the Company relocated one production line to Vietnam, whose goods may enter the United States without quota. The Company intends to enter the United States market with its Vietnamese-produced goods.

The Company has three major competitors in the manufacture of plastic rope in Malaysia, one of which also manufactures fishing nets using such rope. These competitors manufacture ropes in only limited rope sizes, while the company produces ropes in a full range of sizes. The Company believes it enjoys an additional competitive advantage as it produces finished end products requiring no additional processing, whereas the products of its domestic competitors require further processing prior to use. The Company also has a competitive edge over foreign rope manufacturers because Malaysia imposes a 25 % duty on imported plastic rope to Malaysia.

Rubber Bands. The Company is the largest Malaysian rubber band manufacturer with a 90 % share of the Malaysian market, in which rubber bands are widely used in the stationery and packaging industries as well as in households. The Company also exports rubber bands to the Far East, Europe and North. America.

The Company's rubber bands are produced in the rubber band district of Bedong, Kedah, allowing it to receive a constant supply of raw materials including plastic resins, chemical composition and color pigments. It produces an average of 250 tons of rubber bands per month and has the capacity to manufacture a maximum of 300 tons per month. The rubber bands are available in a wide variety of sizes, with diameters ranging from 11mm to 159mm, lengths from 20mm to 250mm, widths from 1mm to 21mm and thicknesses from .9mm. to 3mm. They are available in red, green, blue, yellow, white and black, and standard packaging is 30kg per bag.

The Company's major Malaysian competitor is Central Elastic Corporation Sdn. Bhd., which produces its rubber bands mainly for export. However, Thailand currently is the largest exporter of rubber bands in the world, in part because of the large number of rubber trees located in that country. The Company plans to conduct a feasibility study on relocating its rubber band manufacturing operations to Vietnam to lower production costs and expand its markets by taking advantage of the relaxed trade agreements which Vietnam has with many countries.

Plastic Recycling. In 1994, the Company began recycling used plastics. The Company maintains its own Malaysian plastic recycling facilities in which it recycles 200 tons of plastic each month and has the capacity to recycle up to 400 tons per month. Currently, it has two lines of recycling plastic machines producing off-grade resins (which are approximately 90% virgin grade quality). The off-grade resins are mixed with the virgin grade resins to improve margins. Approximately 30 % of these recycled resins are used by the Company in the production of plastic rope. The balance is sold locally in Malaysia or exported to Thailand.

Industrial Ceramic Products. These products fall into two principal categories: (1) insulators, tubes, rods and crucibles and other labware, all of which are standard catalogue items and (2) machinable ceramics. The products, which are used principally by the aerospace, electronic detection equipment and industrial heating industries, are manufactured by ECS Inc. and by third parties and warehoused and distributed by the Company from its facilities in Briarcliff Manor, New York.

Diamond Cutting Tools. Dicing Blades. Dicing blades are made of diamonds bonded with nickel alloy. They are used with the precision electronic dicing saws which the microelectronics and semiconductor industries use to cut and separate integrated circuits and discrete devices made from silicon and other wafers. The blade market consists principally of hubbed and hubless blades,made of three types of materials, diamond/metal (the most common), diamond/thermoset plastic (called resin blades, which are the blades most widely used in precision electronic saws for cutting ceramic substrate, even though they have a shorter useful life) and sintered metal.

Scribes. Scribes, which have tips made out of gem quality diamonds, are used to cut silicon wafers and perform die and integrated circuit separation. These products, which are assembled in the Company's facility in Briarcliff Manor, New York and Malaysia, have limited growth potential in this application since the electronics and semiconductor industries have in large part switched from scribing machines to dicing saws for the wafer cutting process. However, diamond scribes are preferred over sawing for cutting certain wafer materials because they provide cleaner separation. They also are preferred for certain low volume applications which do not justify the capital expense of using a dicing saw.

Dressers. Dressers are diamond-tipped tools generally used to "dress" or shape abrasive grinding wheels in machine shops. These products, which are assembled in Malaysia are sold by the Company principally to companies which resell them to third parties.

Clean Room Materials and Supplies. These products include cleaning chemicals, latex gloves and other items used to preserve a contamination free environment, and they are primarily marketed to IBM and Lucent Technologies.

FUNDAMENTAL ANALYSIS

Upon review of Select Financial Data located in Box A, investors have the opportunity to see actual and estimated year end numbers and actual first quarter for fiscal 99. For your review, we have calculated three investment standards for 99 and 00 and will demonstrate that SETO, in our opinion, remains extremely cheap. Our variables used in this exercise - PE, PSR and P/CF.

During 99E revenues are estimated to grow by 55% over 98A and 00E is estimated @ 37.5% over 99E. Earnings estimates during that same time period are estimated at 88% and 41%, respectively. If Wall Street had these numbers for a specific opportunity, it is obvious that the stock in question would sport a very high PE valuation. In our opinion, a PE of 35 could not be out of the question. This, of course, in our opinion, would be reserved for the highest of quality and, of course, listing on a major exchange.

In reality, we are relatively conservative and must haircut our opportunity since it does not trade on any listed exchange, it is a mini-micro cap and has limited coverage (we are currently the only financial entity that follows this investment opportunity) by the investment community.

We believe that a PE valuation of 20x fairly represents this opportunity when one considers all the variables of where this company came from, where it is today and, of course, where it will be tomorrow! We usually never value a mini-micro so boldly, but in our opinion, SETO is a no-brainer! If we value SETO based upon a PE of 20x, then our share valuation expands quite rapidly from current levels of .82. At present SETO trades at a PE for fiscal 99 at 4.8x and 3.4x for fiscal 00. Based upon our earnings estimate for 99E and 00E, SETO's share price demonstrates a heavily discounted opportunity that should increase in price as exposure broadens. Our slightly aggressive assumptions concerning PE for SETO yields us a $3.40 share price based upon fiscal 99 and a $4.80 share price for fiscal 00. Based upon the current share price of .82 and an integration of our assumed model, we deserve to see within the next 18 months a share appreciation of 314% to 485%. This is not pie-in-the-sky -- these numbers have been formulated by continual guidance by SETO management.

When examining P/CF estimates for fiscal 99 and fiscal 00, our values are just as compelling. In our opinion, SETO should trade at a P/CF of 10x. This again is not a very aggressive valuation, but still rewards SETO with a premium (as stated, we haircut opportunities due to size of revenue base and quality of listing on exchange) multiple. From Box A our estimated guidance yields a P/CF valuation for 99E and 00E, respectively, 3.9x and 2.9x. If we generate a share valuation based upon a P/CF of 10 instead of current value estimates, then our share price would be $2.10 and $2.80, respectively. This yields an appreciation potential of 156% to 241% within the next 18 months based solely upon P/CF. We believe that PE is the most important investment standard for investment guidance.

It is important to realize that earnings for SETO may expand much more rapidly than estimated in this document. Upon review of the first quarter 10Q, an astute investor should be able to derive from the statement of income that actual operating profits actually exceed $1.5 million, but 800K went to interest expense. Since much of SETO's debt is pegged to the Malaysian prime rate (currently 18%), then debt service will continue to reduce real earnings potential near term. If the interest rate is more in line with US prime value, earnings would increase by at least 50%/year. The company is actively pursuing methods to reduce debt and increase working capital so as to expand more rapidly. It is in our opinion that some form of equity financing during 1998 will occur. Management insists that the dilution will be kept to a minimum. Management has in previous discussions mentioned that NASDAQ listing will be an eventuality and that at some point in time the maximum reverse split for SETO would only be a 2 for 1.

Our last fundamental variable that we will consider is price to sale (PSR). By most standards, a value of under 1 is considered extremely cheap and undervalued, while a value of 3 is considered fairly valued. A more conservative approach concerning PSR is to subtract out debt. Our calculation will be based upon the subtracted out version for SETO. For 1999 and 2000 our estimated valuations are .59 and .40, respectively. We believe that since SETO is an extremely high quality mini-micro, then it should be trading at a PSR of at least 1.5x. This would just make SETO halfway between being fairly valued; that is, to have a value of 3x. At 1.5x SETO's share price would be around $2.50 and $3.50, respectively or 205% and 327% above the current share price of .82/shares.

Any way you slice, dice, rope, tie or recycle SETO, its shares are extremely undervalue based upon PSR, P/CF and most importantly, PE. The values speak for themselves. The fundamental risk here is not owning SETO at current prices as a core holding for all mini-micro portfolios geared toward long term appreciation!

Box A Select Financial Date Years Ended January Fiscal 98A Fiscal 99E Fiscal 00E 1 Quarter 99A April 30 Revenue 25.8 mil 40 mil 55 mil 9.3mil Net Income 1.8 mil 3.9 mil 5.5 mil $734K Net Income/sh .09 .17 .24 .03 PE 9.1x 4.8x 3.4x PSR .63 .47x (4) .34x (4) PACF 3.9x (2) 2.9x (3) Shares Outstanding 20 mil 23 mil 23 mil 23 mil1. Semicon Tools., Inc. acquired Teit Tatt Holding Co. 11/97 - prior to acquisition. Semicon had revenues of $2 mil/yr

2. D & A assumed to be 875K

3. D & A assumed to be 1 million

4. Our PSR valuation has subtracted out current portion of LTD ($8 million) - upon minus the LTD our values are .59 and .40, respectively.

5. All values are in U.S. dollars - most business conducted in dollars.

Box B Fundamental Comparison of Diversified Companies Earnings Est. for PE estimate for

Company SymboL Price current calendar or fiscal year Semicon Tools SETO .82 Jan 99 4.8 (NASDAQ BB) .17 Myers Industrials MYE 21 3/4 Dec 98 16.1x (AMEX) 1.35 Pacific Dunlop PDLPY 5 15/16 Jun 99 9.3x ADR(NDQ) .64 Pontair, Inc. PNR 41 3/16 Dec 98 16.8x (NYSE) 2.45 Thermo Pibertek TFT 11 1/4 Dec 98 21.2x (ASE) .53 Tyco International TYC 54 1/16 Sept 98 36.x (NYSE) 1.50 Average PE valuation for 1.5 19.9x1. MYE operates 2 divisions - manufacturing makes and markets a diverse range of reusable plastic containers, plastics and metal storage/organizers and rubber products to mass merchandisers. the other division distributes tools and supplies used for under-car repair and tire servicing, retreading, and manufacturing.

2. POLDY has five business groups - consumer products, electrical and auto parts, tires, health-care and industrial and electrical. It sells latex gloves, condoms, batteries, clothing, sporting goods and products for the industrial, building and furniture markets.

3. PNR manufactures electrical and electronics enclosures, woodworking equipment, power tools, pumps, automotive service equipment, industrial systems, material dispensing, equipment and water conditiong control equipment.

4. TFT develops, manufactures and markets equipment and products for the papermaking and paper recycling industry, including de-inking systems, stock prepartion equipment, and water management systems.

5. TYC - diverse manufacture - products include fire protection systems, pipes, fittings, underwater communications and power cables; disposable medical supplies and adhesive products, printed circuit boards, paper and plastic packaging products.

FUNDAMENTAL ANALYSIS - Part 2

Within Box B we have decided that it is important to compare SETO to some of its peers. We chose MYE, PDLPY, PNR, TFT and TYC. They are all much larger, well-defined and listed. Our main purpose is to compare SETO's PE to the group's average. Each company mentioned has a brief description listed. Upon review, one can see that the PE estimates are similar for the listed companies. We will compare SETO's PE with the whole group and then drop out the high and low of the group and then average the remaining.

When we compare SETO's estimated PE valuation for fiscal 99, that is 4.8x and the resulting value from the average five candidates, the resulting PE estimate for the group equals 19.9x. If SETO was to trade at a PE multiple of 19.9x estimate 1999, then its current share price would equal $3.38, a huge 312% gain from current levels.

When we compare SETO's fiscal 99 PE estimate of 4.8x to our second valuation; that is, dropping the high and low values and averaging the remaining 3 candidates, a resulting PE estimate of 18x is calculated. If SETO was to trade at 18x, its estimated PE for fiscal 99, its current share price would equal 3.06, a 273% appreciation from current levels.

One final point concerning PE valuations. The trailing 12 months for SETO yields .12/share net income/share. This value yields a trailing twelve month PE of 6.8x. All our preceding calculations indicate to us that SETO should trade at a PE multiple of between 18 and 20. This indicates that SETO, in our opinion, has a 200 to 300% upside potential. It should start to build into the current share price. As exposure intensifies, SETO will most definitely appreciate dramatically. A two dollar stock should be easy!!!

OVERVIEW

Why SETO has been recommended twice and featured during January 1998 as our "Stock Pick of the Year" (@.37) (Note: first recommended 7-9-97 @ .07, and 6-2-98 @ .81).

- The fundamentals of SETO are beyond compelling (trading at 6.8x trail twelve and 4.8x fiscal 99 ending January) - SUPER BULLISH!

- Growth rate anticipated at 49% during the next 2 years - SUPER BULLISH!

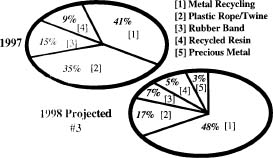

- Metal recycling anticipated to grow by 66% over 1997 - extremely Bullish!

- PC shipments reach an estimated 90+ million worldwide - bodes well for very strong computer recycling as new replaces old. This is one reason recycling will propel SETO's growth at such huge percentage during fiscal 00 or beyond.

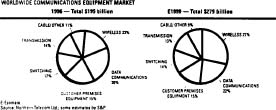

- Other aspects of recycling SETO receives consumer electroncis of all sort and telecommunication and cable equipment. From chart below one can see the supply possibilities are unlimited.

- From pie charts below, should be able to conclude that worldwide communication equipment market will supply SETO with all the recycling material that they can possibly process during fiscal 99. The market size is huge and an endless supply.

- The dicing blades and scribes are primarily used in the semiconductor industry. The continued growth bodes well for this segment of SETO to expand.

- SETO is the largest plastic rope manufacturer in Malaysia, with a 40% market share - Bullish!

- SETO has a 90% market share of rubber bands being manufactured in Malyasia - Bullish!

- More of SETO's present Malaysian manufacturing are beig relocated to Vietnam due to lower production cost and relaxed trade agreement - Bullish!

- Malyasia's real GDP growth anticipated during 1998 at .2%, while SETO's anticipated to grow by 60% - very Bullish!

- SETO conducts the majority of business in US Dollars. The company buys raw material for local currency, but sells products worldwide in US Dollars - very Bullish!

- Management appears extremely competent. Guidance extremely accurate - very Bullish.

- Long-term debt pegged at Malaysian prime at present is around 18% - starves SETO of even greater earnings potential. If debt was in the US, the earnings would grow by an additional 45% - mildly Bearish.

- Anticipate near term equity financing to reduce debt and expand more rapidly - 10% dilution anticipated with restrictions (144 stock held for one year) - Bullish confidence!

- Acquisition oriented - Bullish!

- NASDAQ listing planned within 12 months (would only consider a 2 for 1 reverse stock split for listing) - Bullish!

- Very shareholder friendly - very Bullish!

CORPORATE INFORMATION

Fiscal Year -January 31

Shares outstanding as of April 1998- 23,279,000

Free trading shares - 5 million

Shareholders - 600+

Book value as of April 30 - .37

LTD as of April 30 - $9.5 million

Fully reporting with SEC

Estimated revenues & earnings for fiscal 99 ending January 31 - $40 mil & .17/share net income after taxes & fully diluted based upon 23.2 million shares outstanding.

Estimated revenues & earnings for fiscal 00 ending January 31 - 00 - $55 mil & .24/share net income after taxes & fully diluted based upon 23.2 million

Estimated PE for fiscal 99 - 5.1x based upon current price

Estimated PE for fiscal 00 - 3.6x based upon current price

Employees - 620

Market Cap as of June 10, 98 - $19 mil

Estimated PSR ratio value based upon fiscal 99 - .47

Estimated P/CF valued based upon fiscal 99 - 3.9x

Dividend - None

Legal - None

Growth rate for current year over last est. @ 55%

| Corporate Headquarters SEMICON TOOLS, INC. 554 NO. STATE RD BRAIRCLIFF MANOR, NY 10510 Contact: Gene Pian 914-923-5000 |

Officers & Directors Eugene Pian - President Craig Pian- Vice President & Treasurer Francine Pian- Secretary Tan Khay Swee- 50% Control |

| This investment opportunity is our "STAR". It has the story, management, growth potential and super attractive

fundamentals. SETO is a major core holdings for mini-microcap portfolios. In our opinion, SETO at current levels is a screaming buy. We would

at least own 10K at current price.

We initially recommended SETO at .07 on or about July 9, 1997. We then featured SETO in our January 1998 newsletter as our (.33) stock pick of the year "for 1998 for Dick Davis Digest." We then re-recommended SETO on June 2, 1998 at .81. We are currently monitoring SETO in our Summer Portfolio 1997 #1 and #21 for percentage gain performance and our e-mail portfolio. Broker contacts: Mike Chesler - 1-800-331-1355 Greg Nelson - 1-800-269-9460 |

| S.A. Advisory, an advisory firm, acts as a consultant to SETO. We have been paid for the production of this anecdotal research report We may have purchased shares in this issue and may sell or buy additional shares at our own discretion. Before investing, consult the latest 10Q and/or call the company for any questions that you may have concerning SEMICON TOOLS, INC. SETO SA Advisory's Home Page: http://www.saadvisory.com |